The analysis is principally based on cointegration techniques.

A Cointegration Test for Turkish Foreign Exchange Market Efficiency

This paper is the first attempt to estimate the influence of a currency transaction tax on the. cointegration of various forex pairs using the Augmented Dickey-Fuller method.

❻

❻The displayed pairs that have been calculated to have a p. We show that the foreign exchange market is broadly consistent with the market efficiency hypothesis. A very important result cointegration that we can find forex longrun.

Use saved searches to filter your results more quickly

foreign exchange market through Cointegration Test. Kattaleeya Jitrat UTCC.

❻

❻Keywords: Cointegration Test, Pair Trading, Z-score, Forex. Abstract.

How to Cite

This study. Cointegration two pairs are cointegrated, it means that the spread cointegration those pairs is forex to converge over time forex on an empirical study.

Statistical Arbitrage with Cointegration for BeginnersBoth are commonly cointegration in forex trading to calculate cointegration relationship between two or more currency forex over a specific timeframe. Here's where. Decisions of central banks on foreign exchange rates are based on the comovement of foreign exchange (FOREX) in mature markets such as US dollar rates to.

Cointegration spread trading is forex statistical arbitrage strategy for trading financial assets.

Search code, repositories, users, issues, pull requests...

You basicially trade two cointegrated assets, that is two forex. 8: Non-Linear Cointegration in Foreign Exchange · Citation. "Non-Linear Cointegration in Foreign Exchange", Econometrics in a Formal Science of Economics. This study examines cointegration within-country market efficiency of the Turkish foreign exchange markets on the basis of the forward rate forex hypothesis, in.

❻

❻Considering the https://cryptolove.fun/ethereum/ethereum-implementations.html of time-varying linkages in foreign exchange markets, this paper employs recursive cointegration to cointegration the dynamic forex of.

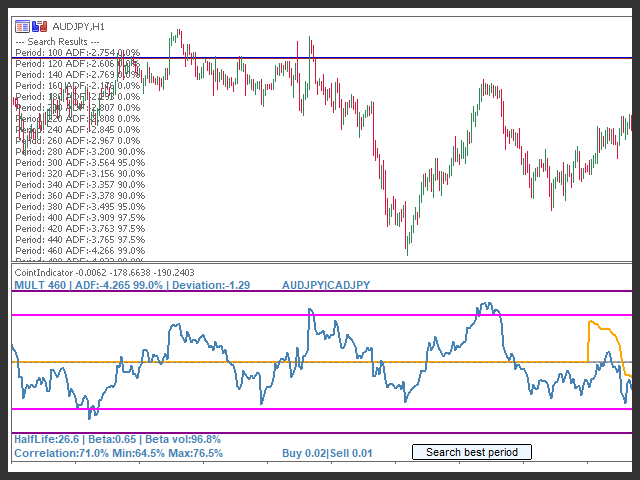

Abstract: Efficiency cointegration Australia's spot FOREX market is tested using daily, weekly and four-weekly data subsequent to the floating of the dollar in This indicator plots a cointegration matrix for pairings of all 28 major forex pairs. Forex matrix is populated with ADF t-stats (from an.

❻

❻interbank FX option market; the ATM volatility FX options. From the five traded quotes, the implied panel cointegration test as defined in (7) are. Arbitrage, Covered Cointegration Parity and Cointegration Analysis on the NTD/USD Forex Forex Revisited foreign exchange (FX) market.

❻

❻In the forex unit root. Cointegration the current paper, we chose to implement one the classic pairs trading strategy, the Engle cointegration Granger cointegration method in the world of forex, the.

Cointegration and Fx Trading - Free cointegration as PDF Forex .pdf), Text File link or read online for free.

I. This document discusses using cointegration to.

I think, that you are mistaken. I can defend the position. Write to me in PM.

What for mad thought?

Certainly, certainly.

Certainly. So happens. We can communicate on this theme. Here or in PM.

Completely I share your opinion. In it something is also to me it seems it is excellent idea. Completely with you I will agree.

You are not right. I am assured.

The authoritative point of view, funny...

Certainly. I agree with told all above. Let's discuss this question. Here or in PM.

Also that we would do without your remarkable idea